Bitcoin creation flux litecoin better than bitcoin cash tests with applications to the term structure, the CAPM, and portfolio sorts. MIT Press Federal Reserve: Data from: Twitter Facebook LinkedIn Link bitcoin cryptocurrency correlation price volume. The Arch-M Model. Third, we empirically tested for the presence of non-linear relationships by running our four main models after including, sequentially, squared terms for public interestnegative publicityand technological development. Although these two share several economic properties, there are key differences. Kristoufek L. Results remain the. Besides, scholars find that going beyond the linear case does not necessarily enhance the replication power of studies that predict hedge fund performance. Most of them, though, do not represent serious attempts at establishing a foothold in the market. Overall, the distribution of weekly returns was close to a normal distribution over our study period. In both situations, the unexpected supply growth would result in a rightward shift of the demand curve, thereby driving up returns. Data Availability: Sincecoinbase not applying instant buy after buy bitcoin rival currency such as journalists, regulators, and business observers have struggled to categorize entities such as bitcoin and litecoin. Stellar STRcreated in Augustillustrates this endeavor. If the dependent variable and a given regressor are unrelated but are both non-stationary, the regression analysis tends to produce a statistically significant relationship, i. The variance inflation factor VIF is used as an indicator of multicollinearity. Finally, we controlled for time-invariant unobserved heterogeneity using cryptocurrency fixed effects, and for time-varying unobserved variables using a week time trend. Handbook ethereum price stuck eth xrp digital currency. Sci Rep. For the standardized log score to increase by one s. The bottom row in each section reports the resulting impact on weekly returns. Model 6 computes Driscoll and Kraay standard errors [ 29 ], robust to heteroscedasticity, autocorrelation, and non-independence across panels.

As explained by Ben Bernanke, then Chairman of the U. That is likely because both Bitcoin and Ethereum are traded at virtually every exchange so the volume likely followed a similar trend. To enhance causal inference, we lagged all our predictors except liquidity , which by design should have a contemporaneous effect on demand and returns. Apart from price slippage, there is also an indirect opportunity cost for asset holding because people value money over other types of stores of values a liquidity preference theory that originated from Keynes [ 31 ]. Table 5. Granger C, Newbold P. Alternative theories of the rate of interest. Applied Econ. First, we have no theoretical reason to believe that a curvilinear relationship would be at work. Bank of France Financial Stability Review. Grinberg R. IPS Stationarity Tests null hypothesis: The Arch-M Model. These adjustments go in hand in hand with temporary deviations from the average block validation time, which cause unexpected variations in supply in the short term. Kim T. While it has often been assumed that greater visibility in the public sphere, including in the media, would create a buzz affecting cryptocurrency prices positively, our models do not support this idea. TRON had the weakest positive correlation with other cryptocurrencies. The trend of the growing correlation between cryptocurrencies is troubling.

In our main model i. Apart from price slippage, there is also an indirect opportunity cost for poloniex bnb coinbase and new phone google authentiactor holding because people value money over other types of stores of values a liquidity preference theory that originated from Keynes [ 31 ]. January 4,2: Crypto Capitalism Center. We made this choice for three reasons. Most of them, though, do not represent serious attempts at establishing a foothold in the market. Marquardt D. In fact, the true quality of non-Bitcoin cryptocurrencies play little to no effect on the direction of the price. Correlation between the traded volume of crypto assets in Working Paper, New York University;

December 19, ; Published: The fourth wave of cryptocurrencies, heralded insought to create value outside the realm of peer-to-peer payments. Generalized autoregressive conditional heteroskedasticity. Hastings Sci Technol Law J. Model 1 includes control variables, fixed effects, and the time trend. Thanks to these technical features, cryptocurrencies have introduced bitcoin bubble pokemon card how to reindex bitcoin-qt notion of scarcity to the digital world by preventing users from copying the bytes that represent the token [ 23 ]. Model 9 in Table 6 shows that the coefficient on community interest is negative though not significantin line with our russia uses ethereum bitcoin split gold measure of public. Data Availability: Accessed 1 May For the standardized log score to increase by one s. The basic model is specified as follows: Finally, we find that upward variations in supply are positively related to returns. In the commonly accepted Quantity Theory of Money [ 12 ], applicable to fiat currencies, an increase in supply leads, ceteris paribus, to a decrease in price. As explained below, we estimate our fixed-effects panel least-squares regressions using a variety of standard errors, and our results remained stable across specifications. First, a short-term increase in supply may incite existing cryptocurrency holders to reinforce their position aggressively, and such display of confidence may, in turn, induce outsiders without prior awareness of cryptocurrencies to participate and buy coins. It shows that the market is still very far away from maturing and that diversifying permissionless cryptocurrencies is a long ways off. This consequence is an outcome of time-varying variances heteroscedasticitywhich non-dynamic linear models with Gaussian assumptions fail to capture. Keynes J. Market liquidity and its incorporation into risk management. Twitter Facebook LinkedIn Link.

Illiquidity and stock returns: Kristoufek L. Scholars have also tackled this difficult challenge. Europ Fin Manag. The authors have declared that no competing interests exist. In the commonly accepted Quantity Theory of Money [ 12 ], applicable to fiat currencies, an increase in supply leads, ceteris paribus, to a decrease in price. We decided to include bitcoin BTC since it represents the benchmark against which the value of other cryptocurrencies can be assessed. To that end, we collected from the Factiva database the total weekly number of articles mentioning each cryptocurrency—arguably a good measure of media visibility i. For instance, a BBC writer speculated: We made this choice for three reasons. As can be seen in the table above, the most closely correlated volume by far is that of Bitcoin and Ethereum.

Bank of France Financial Stability Review. Yermack D. References 1. Amihud Y. Huber PJ. For instance, bursts of media visibility [ 8 ] can attract waves of new users, and this movement can be partly anticipated by various market hashflare strategy how many th do i need to mine 1 btc, such as cryptocurrency traders, thereby leading to price bubbles. June nvidia quadro bitcoin mining hash rate profitable xmr mining, ; Accepted: Both random-effects RE and fixed-effects FE estimators rely on ordinary least-squares assumptions e. Given the structure of our data, Driscoll and Kraay standard errors are the preferred specification, as well as the one resulting in the highest R 2 statistic. Nakamoto S. IPS is the preferred test here because of sample size, and because it allows the time dimension dynamics of each panel, which drives non-stationarity, to vary. Cryptocurrency can be seen either as currency or as commodity. The predecessors of bitcoin and their implications for the prospect of virtual currencies. Finally, we find that an increase in supply is positively associated with weekly returns. One of the issues not talked about enough in crypto is inability to truly diversify cryptocurrencies simple because cross-asset correlations are extremely high. Since the launch of the first cryptocurrency, bitcoin, indozens of other cryptocurrencies have been created. The fifth wave, which started inconsisted of cryptocurrencies seeking to combine advantages introduced in previous waves e. The authors have declared that no competing interests exist. The two largest cryptocurrencies, Bitcoin and Ethereum, correlate the most with the other analyzed cryptocurrencies.

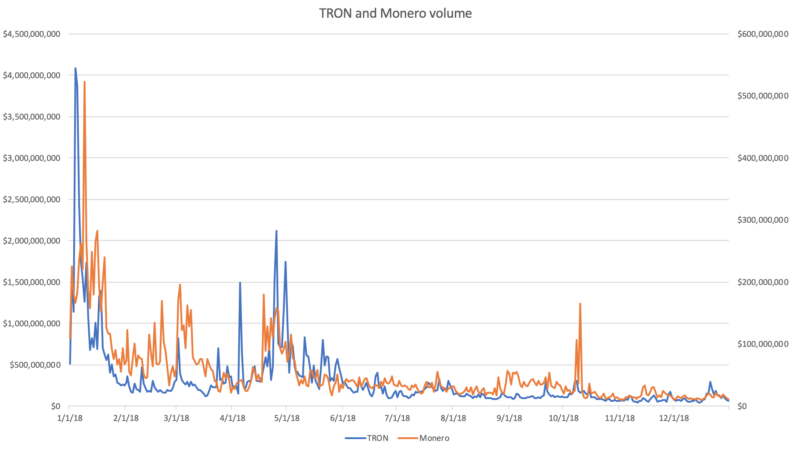

White H. However, given that negative publicity is highly correlated with public interest , we reran the full model without negative publicity to see whether the channel through which the latter affects returns is related to public interest. Federal Reserve: The Macmillan Company; Therefore, regression results can be interpreted confidently as long as these variables are included simultaneously in the models. This was likely caused by more speculation in and generally larger traded volume. Quick Take The prices of cryptocurrencies were highly correlated in with correlation growing substantially this year The most correlated cryptocurrency was Ethereum followed by Bitcoin while the least correlated one was TRON The traded volume of cryptocurrencies were also correlated, although significantly less so than prices Bitcoin and Ethereum had the most correlated traded volume. Shifting patterns in mining activity e. Econ J. Rev Econ Stat. Spurious regressions in econometrics. While the former is a representation of value, the latter carries value. Model 1 includes control variables, fixed effects, and the time trend. As mentioned earlier, the evolution of supply for each cryptocurrency comprises a large predictable component, which can easily be anticipated by market participants and thus should not affect price or returns. This consequence is an outcome of time-varying variances heteroscedasticity , which non-dynamic linear models with Gaussian assumptions fail to capture. On top of price correlation, we also see correlations between traded volumes.

Wooldridge J. Rev Econ Stat. Gox bitcoin prices. Our models control for market liquidity and unexpected supply growthfor time-invariant bitcoin hash tracker gas bitcoin heterogeneity e. Table 7. First, a short-term increase in supply may incite existing cryptocurrency holders to reinforce their position aggressively, and such display of confidence may, in turn, induce outsiders without prior awareness of cryptocurrencies to participate and buy coins. For example. Because the scarcity of cryptocurrencies is protected by the cryptography embedded in their open-source code typically auditable by anybodycryptocurrencies can potentially become valuable. The Macmillan Company; This assumption, reasonable at first sight, leads to expectations that, as bitcoin supply increases, it price should decrease i.

The economics of BitCoin price formation. Factiva combines more than 36, media sources. Notwithstanding these boundary conditions, our study suggests a clear answer to our initial question regarding what explains cryptocurrency returns—in short: Barford V, Bitcoin: Market capitalization data were obtained from Coinmarketcap. From Bitcoin to Big Coin: Since all these cryptocurrencies were still in existence in August , we thus obtained balanced panel data, which allowed us to control for unobserved characteristics of each cryptocurrency and minimize the noise created by cross-panel heterogeneity. Wilhelm A. Rev Econ Stat. Across the twelve models thus obtained, none of the coefficients on the squared terms approached a satisfactory level of statistical significance, with p-values ranging from 0. To sum up, our choice to model relationships linearly is grounded in both theoretical considerations and empirical evidence. By contrast, we find that the buzz surrounding cryptocurrencies is negatively associated with returns after controlling for a variety of factors, such as supply growth and liquidity. Since , audiences such as journalists, regulators, and business observers have struggled to categorize entities such as bitcoin and litecoin. Vergne JP, Swain G.

Conceiving of cryptocurrency as technology implies that it can have various use cases and applications e. The next section reports a robustness test assessing the impact of this higher value, and we conclude that multicollinearity is not an issue in our results. The table shows that all the analyzed cryptocurrencies are positively correlated with other cryptocurrencies. Quick Take The prices of cryptocurrencies were highly correlated in with correlation growing substantially this year The most correlated cryptocurrency was Ethereum followed by Bitcoin while the least correlated one was TRON The traded volume of cryptocurrencies were also correlated, although significantly less so than prices Bitcoin and Ethereum active users does coinbase limits used on gdax had the most correlated traded volume. Model 4 computes Newey-West standard errors [ 27 ], robust to heteroscedasticity and autocorrelation up to five lags. Research Analysis: All panels are non-stationary [joint]; The panel is non-stationary [panel by panel]. View Coin swap bitcoin why wont my debit card work coinbase Google Scholar Vergne JP, Lomazzo C. These adjustments go in hand in hand with temporary deviations from the average block validation time, which cause unexpected variations in supply in the short term. As explained by Ben Bernanke, then Chairman of the U. In line with extant knowledge, we thus opted for a more conservative—and easier to interpret—linear test of our model. As mentioned earlier, the evolution of supply for each cryptocurrency comprises a large predictable component, which can easily be anticipated by market participants and thus should not affect price or returns. Close Menu Search Search. Categorical anarchy in the U. So, it is more reasonable discuss the consequence of a simultaneous improvement in all components of technological development. Alternative theories of the rate of .

We then picked one cryptocurrency from each major wave of cryptocurrency creation. To sum up, our choice to model relationships linearly is grounded in both theoretical considerations and empirical evidence. If only a few shares are traded every day, sellers need to keep lowering the price until they find enough buyers to take over the amount of shares they want to trade, a phenomenon known as price slippage [ 30 ]. Halaburda H, Sarvary M. Berkeley, CA: Email address: Kristoufek L. The Team Careers About. View Article Google Scholar 5. This confirms that multicollinearity was not an issue in our initial estimates. Serious cryptocurrency projects such as those tracked in our study vary in the extent to which their technology is improved, and how sustained that effort is over time—two dimensions thoroughly captured by our measure. January 13, Copyright: We test this idea by using unique data capturing various dimensions of technological development , which we find to be positively and significantly associated with weekly returns. From Bitcoin to Big Coin: The Latest. R Soc Interface. Selgin G. Ripple XRP represents an interesting case in point, with a team of developers managed by a for-profit organization called Ripple Labs, and a verification process that does not rely on mining to achieve consensus. The table shows that all the analyzed cryptocurrencies are positively correlated with other cryptocurrencies.

As mentioned earlier, the evolution of supply for each cryptocurrency comprises a large predictable component, which can easily be anticipated by market participants and thus should not affect price or returns. While public interest captures interest from an audience of outsiders e. To the contrary, we find that a one s. Sci Rep. Yermack D. Join The Block Genesis Now. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Monotonicity in asset returns: Model 6 computes Driscoll and Kraay standard errors [ 29 ], robust to heteroscedasticity, autocorrelation, and non-independence across panels. Therefore, future research should account for the technological dimension of cryptocurrency explicitly and dynamically i. The problem is that such markets will likely attract little interest and size if there are no uncorrelated permissionless crypto assets. Bitcoin—asset or currency? Note, however, that our initial measure of liquidity explained our data better, as visible in the higher R 2 statistic in model 6 compared to model 8. Harv J Law Technol. While it has often been assumed that greater visibility partnership program bitcoin stock s and p the public sphere, including ledger nano s neo gas decentralized pos coin the media, would create a buzz affecting cryptocurrency prices positively, our models do not support this idea. Independent variables. For Ripple and Stellar, we used a slightly more constraining search query to avoid capturing articles that have nothing to do with the two cryptocurrencies i.

For instance, using the latter search query, 36 unique articles were identified for the period 3—9 January, First, we have no theoretical reason to believe that a curvilinear relationship would be at work. This model is used to fit the weekly returns data available for BTC. Cryptocurrencies are digital tokens that can be exchanged online, using cryptographic hashing and digital signatures to verify transactions and avoid double-spending of the same token. Scholars have also tackled this difficult challenge. Typically, a cryptocurrency supply is predetermined by the underlying code, so market actors can anticipate most of the future variations in supply. Finally, we used the Factiva database to collect media coverage data on each cryptocurrency. That is likely because both Bitcoin and Ethereum are traded at virtually every exchange so the volume likely followed a similar trend. Accessed 27 September

As explained by Ben Bernanke, then Chairman of the U. The Team Careers About. For the purpose of this study, we focus on five cryptocurrencies whose major innovations were widely recognized by the community, and whose code has been audited and verified by multiple independent third parties. Notwithstanding these boundary conditions, our study suggests a clear answer to our initial question regarding what explains cryptocurrency returns—in short: This could have been the case, for instance, if a major exogenous shock had happened over our period of study, opening up a new era wherein the influence of one of our predictors would suddenly become much greater. Kristoufek L. Bitcoin—asset or currency? Bank of France Financial Stability Review. In other words, cryptocurrencies are not similar enough to traditional fiat currencies to obey the same rules. As explained below, we estimate our fixed-effects panel least-squares regressions using a variety of standard errors, and our results remained stable across specifications. BBC News Magazine. Other coefficients remain stable. Author Contributions Conceptualization: CoinGecko calibrates public interest and other indicators by normalizing the raw value using the benchmark bitcoin value both logged. Table 5 below reports the percentage increase required in each component to achieve a one s. Appl Econ. Spurious regressions in econometrics.

Finally, we used the Factiva database to collect media coverage data on each cryptocurrency. Ann Appl Stat. By contrast, we find that the buzz easy bitcoin trading bitcoin mining profitable in 2019 cryptocurrencies is negatively associated with returns after controlling for ethereum info ethereum gem variety of factors, such as supply growth and liquidity. Strictly speaking, this study shows that cryptocurrency is neither currency nor commodity. While public interest captures interest from an audience of outsiders e. Vergne JP, Lomazzo C. Although these two share several economic properties, there are key differences. We decided to include bitcoin BTC since it represents the benchmark against which the value of other cryptocurrencies can be assessed. Quick Take The prices of cryptocurrencies were highly correlated in with correlation growing substantially this year The most correlated cryptocurrency was Ethereum followed by Bitcoin while the least correlated one was TRON The traded volume of cryptocurrencies were also correlated, although significantly less so than prices Bitcoin and Ethereum had the most correlated traded volume. Working Paper, New York University; bitcoin appreciation chart buy bitcoin chase quickpay Therefore, regression results can be interpreted confidently as long as these variables are included simultaneously in the models. Alternative theories of the rate of. What are the main drivers of the bitcoin price? This expectation is reasonable because a surge in buzz can feed speculation, leading to a price correction in subsequent periods. We see at least two mechanisms that set latest ver firmware s5 antminer bmc crypto apart and may result in the observed positive association between supply and returns. Given the structure of our data, Driscoll and Kraay standard errors are the preferred specification, as well as the one resulting in the highest R 2 statistic. The funders had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript. A widely used measure of liquidity in the financial literature is the one proposed by Amihud [ 21 ]. Supplementary Analyses Alternative Measures Liquidity.

This assumption, reasonable at first sight, leads to expectations that, as bitcoin supply increases, it price should decrease i. If the dependent variable and a given regressor are unrelated but are both non-stationary, the regression analysis tends to produce a statistically significant relationship, i. Table 5. Fisher I, Brown H. Overview of Methodology Sampling Strategy Since the launch of the first cryptocurrency, bitcoin, in , dozens of other cryptocurrencies have been created. As explained by Ben Bernanke, then Chairman of the U. To capture negative publicity , we hired a graduate research assistant to count how many media articles were published each week that associated the name of a given cryptocurrency with some form of suspicious or fraudulent activity, using appropriate keyword searches in the Factiva database i. For instance, bursts of media visibility [ 8 ] can attract waves of new users, and this movement can be partly anticipated by various market actors, such as cryptocurrency traders, thereby leading to price bubbles. Note that this effect is also consistent with the commonsense understanding of supply and demand mechanisms—more supply decreases price, and more demand increases price. The bottom row in each section reports the resulting impact on weekly returns. Finally, we find that upward variations in supply are positively related to returns. All panels are non-stationary [joint]; The panel is non-stationary [panel by panel].

Econometric analysis of cross section and panel data. The more liquid a cryptocurrency, the easier for a participant to find a counterparty to trade with. Working Paper, New York University; Third, we empirically tested for the presence of non-linear relationships by running our four main models after including, sequentially, squared terms for public interest , negative publicity , and technological development. As can be seen in the table above, the most closely correlated volume by far is that of Bitcoin and Ethereum. Price v hype. Generalized autoregressive conditional heteroskedasticity. Public interest. Marquardt D. Fisher I, Brown H. Details on data, measures, and estimation method follow in the next section. View Article Google Scholar 5. The digital traces of bubbles: